If you've been on both sides of an M&A transaction, you already know that buy-side due diligence and sell-side due diligence aren't mirror images.

Buyers and sellers approach the diligence process with different goals, different information, and different levels of risk. Buyers want to identify problems before they write a check. Sellers want to present their business clearly enough that buyers can move quickly without second-guessing everything.

See also: How to buy a business: Acquisition guide

The disconnect shows when each side assumes the other is working from the same playbook. A seller thinks that providing access to a data room means the buyer will review everything methodically and possibly ask some questions. A buyer expects the seller to have anticipated every concern and organized documents accordingly. Neither assumption holds up in practice.

According to research, 70-75% of M&A deals fail, and poor due diligence is often to blame.

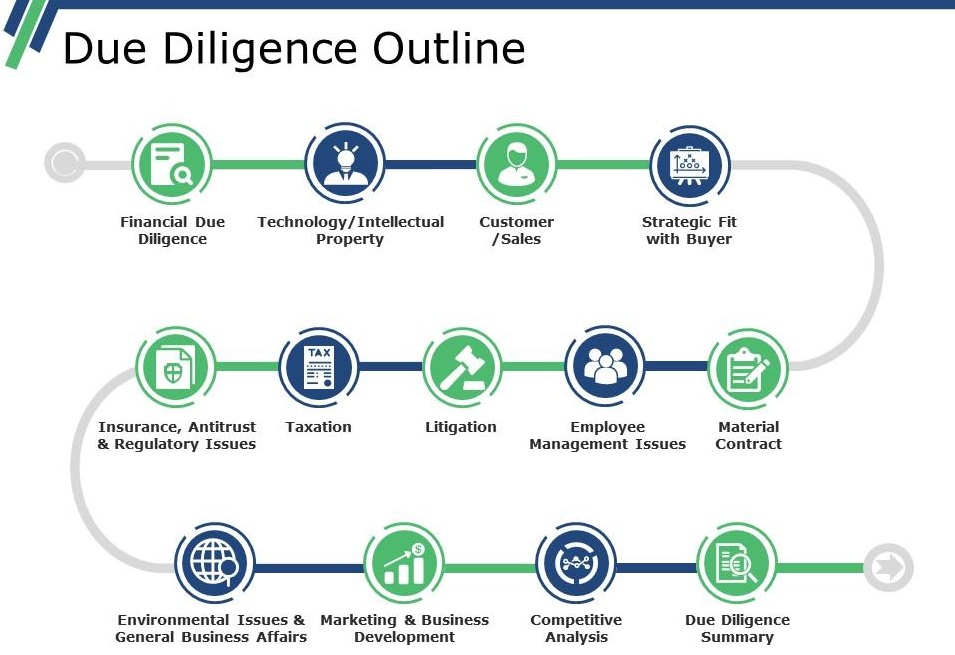

Buy-side teams evaluate risks they'll inherit after the deal closes. Their diligence aims to uncover potential weaknesses in financial performance, customer relationships or operational structure. They're looking at the target company's working capital, cash flow, tax matters and market position with fresh eyes. Every document gets tested against the question: does this change our valuation and the value we're willing to pay?

Sell-side due diligence team prepares materials that help potential buyers understand the business without getting stuck on minor inconsistencies or formatting issues. The goal is to address weaknesses proactively so they don't derail the sale process. When conducting sell-side diligence, you're building the case for why your company's financial information, operations, and market position justify the asking price and potentially deliver maximum value to buyers.

The incentive structures don't align either. Private equity firms and other buyers benefit from finding issues that justify a lower price or better terms. Sellers benefit from helping buyers move through diligence quickly and confidently. Investment bankers working on the sell-side want to avoid surprises that slow momentum or scare off bidders.

Neither side is wrong in their approach. They're just optimizing for different outcomes of the same transaction.

How buyers review documents during M&A due diligence

Here's what most sellers don't realize: buyers don't read documents in the order you would.

They begin with financial statements and then jump straight to anything that looks inconsistent. Maybe revenue recognition changed between years. Maybe customer concentration is higher than the teaser suggested. Maybe the company's financial information shows different margins than the management presentation.

Buyers revisit the same files multiple times. They'll pull tax returns, then circle back after reviewing contracts to confirm what they saw earlier. They'll compare what management said in the Q&A log against what the financial records actually show. It's never linear.

This frustrates sellers who think they've provided complete information upfront. But buyers aren't trying to be difficult. They're building a mental model of the business, and that model gets refined each time they find new information. What seemed clear in week one might raise questions in week three after they've reviewed the customer list or talked to operational teams.

Buyers also prioritize differently. You might think your growth strategy deck matters most. Buyers care more about whether historical financial performance matches what you've projected for the future. They want to see proof, not promises.

The buyer's diligence team will flag anything that raises assumptions. For example:

- How much of the cash flow depends on one customer?

- What happens if a key employee leaves?

- How certain are those market conditions you're counting on?

The more clearly you help them evaluate those risks, the faster they can move toward closing.

See also: Best client database software tools

The sell-side role in keeping due diligence moving

Now, most sellers think their job ends once the data room is live. We hate to break it to you...

Buyers send questions throughout diligence. Some are just asking for missing documents. Others reveal confusion about how your business operates.

At this stage, fast responses matter more than perfect responses. Every delay raises concerns about your operational discipline. If a buyer asks for a breakdown of marketing costs and you need two days to compile it, say so. If you can send a rough version today and a detailed version tomorrow, do that. Silence makes buyers nervous. When they can't get answers, they start wondering what you're hiding.

Document clarity matters just as much, so buyers can find what they need without asking. Label documents consistently. Group related files together. Include summaries or indexes for complex sections. The easier you make it to navigate your business, the fewer follow-up questions you'll get.

It's good to be proactive here. If your revenue declined in Q2 of last year, include a brief memo explaining why. If you changed accounting firms, note when and why. If there's a litigation history, provide the settlement details and confirmation that it's resolved. Every unexplained anomaly becomes a red flag until you address it.

The best sellers prepare a Q&A log before buyers even ask questions. They know which parts of their business will confuse outsiders. They document the answers in advance. Explain problems clearly before they become potential deal-breakers.

Where buy-side due diligence processes and sell-side expectations commonly clash

The first clash happens around timing. Buyers want access to everything immediately so they can assess risks early and identify concerns. Sellers want to stage information (basic materials first, sensitive details later) to maintain some control over the sale process.

Buyers interpret staged access as a sign that sellers are hiding problems. Sellers see demands for immediate access as overreach before terms are even agreed. The compromise usually involves granting earlier access than sellers prefer in exchange for buyers agreeing to reasonable confidentiality protections.

Document completeness creates another friction point. Sellers think they've provided everything relevant. Buyers find gaps and ask for more. The seller's finance team might consider certain details immaterial. The buyer's diligence team considers them critical for valuation.

This happens most often around contracts, customer data, and operational metrics. A seller uploads the top 20 customer contracts. Buyers want all customer contracts above a certain threshold. A seller provides annual financial statements. Buyers want quarterly breakdowns and monthly operational reports to conduct a complete assessment.

Follow-up questions compound the problem. Buyers ask questions based on their review. Sellers answer those specific questions. Buyers then ask follow-ups based on those answers. Sellers get frustrated because it feels like the questions never end. But from the buyer's perspective, each answer reveals new areas that need exploration to properly evaluate the business.

Access to people creates yet another challenge. Buyers want to talk to the management team, key employees, and sometimes customers. Sellers worry about disrupting operations or tipping off employees about a potential sale. The solution usually involves carefully managed calls where the seller is present, but this requires significant coordination and structure.

Deal teams on both sides underestimate how much time diligence will require from operational staff. The finance team still needs to close the books each month. The legal team has regular business to handle. Pulling people away for diligence requests creates strain.

Market conditions add pressure. In a competitive sale process, buyers know other bidders are reviewing the same information. They want to move quickly but thoroughly. Sellers want buyers to move quickly, period.

Preparing documents with both sides in mind

The recipe for successful transactions is when sellers prepare materials as if they were buyers reviewing their own business, bringing both expertise and an objective view to the process.

That means organizing your data room the way a buyer's diligence team will actually use it. Group financial information together. Put all contracts in one section. Create clear folders for legal, operational, and commercial due diligence materials. Include a master index that explains what's where. A well-organized data room in M&A signals operational maturity. When documents are well-managed, clearly labeled, consistently formatted, and easy to navigate, buyers spend less time searching and more time evaluating.

Think about the questions buyers will ask. If your customer concentration is high, prepare an analysis showing customer retention rates and the strength of those relationships. If your market position has shifted, document why and what it means for future growth. If working capital fluctuates seasonally, explain the pattern so buyers can properly assess the value and risks.

When buyers can evaluate risks confidently, they can move to offers faster.

This preparation benefits the seller by forcing you to confront weaknesses in your own business. Finding these issues early gives you time to address them or at least prepare clear explanations. It also reduces the chance of deal-breaking surprises. The worst time to discover a tax liability or regulatory concern is during final diligence.

Check out our detailed M&A due diligence checklist for a comprehensive review of what buyers expect.

Keep in mind that you're also demonstrating how you operate under pressure, communicate complex information, and handle scrutiny. That's equally insightful for buyers and can impact your maximum value.

FAQs

What is the difference between buy-side and sell-side due diligence?

The key difference is incentives: buyers benefit from finding problems, sellers want the best price and buyer confidence.

Buy-side due diligence identifies risks and weaknesses that buyers will inherit after closing. They check financial performance, customer relationships, operational structure, and market position. Their goal is to uncover issues that justify better terms or a lower price.

Sell-side due diligence helps buyers understand the business quickly and confidently. Rather than hiding weaknesses, sellers should address them proactively to prevent deal delays. The goal is to organize financial information, operations, and market data to justify the asking price.

How long does it take to perform sell-side and buy-side M&A due diligence?

Timelines range from six weeks to six months, depending on deal complexity, responsiveness, and preparation quality.

Fast, clear responses accelerate the process, while delays, document gaps, and unexplained anomalies extend timelines. Competitive sale processes often move faster as buyers work to outpace other bidders, while complex businesses with multiple locations or product lines naturally require longer review.

Can a deal fail during the due diligence phase?

Yes. Deals can fail when buyers discover undisclosed liabilities, financial performance that doesn't match projections, regulatory concerns, or lose confidence due to seller unresponsiveness. The most painful failures are late in the process, such as unexpected tax liabilities, customer concentration risks, or operational dependencies on key personnel. Solid preparation and transparency reduce this risk.

What documents do buyers request during due diligence?

Buyers request comprehensive documentation across financial, legal, and operational categories, e.g.:

- financial statements

- revenue recognition details

- cash flow statements

- litigation history and settlements

- intellectual property documentation

- regulatory compliance records

- customer lists and retention data

- market analyses

- historical growth metrics

Buyers also request explanations for anomalies, such as revenue fluctuations, accounting changes, or shifts in market position.